The global K12 education market has witnessed significant growth driven by the implementation of government programs and the increasing use of learning analytics in the educational sector. However, the COVID-19 pandemic and the subsequent shutdown of schools posed challenges to the industry’s growth. Despite these obstacles, the market is expected to rebound due to the rising popularity of adaptive learning, which offers benefits such as formative assessment, mastery-based learning, and efficient feedback mechanisms.

The global K12 education market is projected to reach $525.7 billion by 2031, with a compound annual growth rate (CAGR) of 17.7% from 2022 to 2031. Private schools, which have adopted the K-12 model, are expected to dominate the market. On-premise deployment mode currently holds the largest share, but the cloud segment is forecasted to exhibit the fastest growth due to its cost-effectiveness and accessibility.

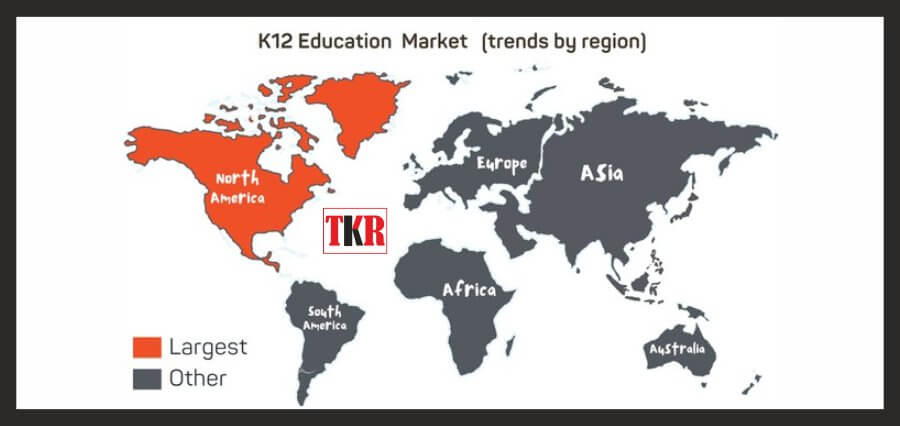

Hardware currently contributes the largest share in terms of spend analysis, while software solutions are expected to witness the fastest growth rate. North America leads the market, driven by the region’s advanced education system, emphasis on reducing administrative burdens, increased investment in educational technology (EdTech), and demand for personalized learning. The Asia-Pacific region is expected to experience the highest growth rate, primarily due to the widespread adoption of online learning.

Key players in the K12 education market include McGraw-Hill Education, Pearson Education Inc., Cengage Learning India Pvt. Ltd., K12 Inc., Blackboard Inc., Tata Class Edge, Educomp Solutions, Next Education India Pvt. Ltd., Adobe Systems, and TAL Education Group.

Overall, the global K12 education market is poised for growth, driven by technological advancements, government initiatives, and the increasing demand for personalized and adaptive learning solutions.